A good financial plan should include the creation of an adequate ‘emergency fund’. This is money that’s kept in an easily accessible account so that you can cover life’s unexpected, and often unwanted, expenses.

Because emergency money needs to be kept in easy to access accounts, this typically means cash savings. That said, this could have implications for your wealth, especially if you have an ‘emergency fund’ that’s too big for your needs.

Read on to discover more about emergency funds, and why holding too much money in one could be dangerous to your wealth.

Why do I need an emergency fund?

In short, an emergency fund is a financial lifeline when life throws you a curve ball. This could be, for example, if you’re diagnosed with a serious illness and not able to work, or an expensive bill, such as a major repair to your house or car.

Emergency funds provide a financial buffer that means you’re less likely to use credit cards or take out a loan to deal with the expense. Either of these could result in expensive charges or interest, which could significantly increase the overall cost of dealing with the problem.

In addition to this, having an emergency fund reduces the need to sell your investments to cover the cost, which could put your financial security at risk. This could be especially true if you have to sell your investments during a stock market downturn, as there is a greater chance of losses.

How much should I have in my emergency fund?

The amount you need in your emergency fund will largely depend on your circumstances and how much you’re comfortable having in it. Some people feel better with larger amounts in their fund, but broadly speaking, you should have enough to cover your essential expenditure for three to six months.

If you’re wondering how much you should have in your emergency fund, the following calculator could help.

Your emergency fund should be held in an easy to access cash account, which is separate from your main current account. The latter ensures you won’t inadvertently spend some or all of your emergency fund, which could create problems if the unexpected happens.

As you need to be able to access your fund at a moment’s notice, avoid putting it into an account that has a long notice period for withdrawals, or has withdrawal fees.

Why shouldn’t I have as much money as possible in my emergency fund?

While you should ensure you have sufficient cash in your fund, care needs to be taken not to have too much in it. This is because your emergency fund needs to be kept in cash accounts for ease of access, which typically offer lower levels of potential growth when compared with investing.

Worse still, money in cash accounts has the potential to drop in value in real terms because of inflation. This measures the rising cost of goods and services over time, which reduces your money’s future spending power.

To illustrate how inflation devalues wealth in real terms, you might want to consider the Bank of England's inflation calculator. It reveals that you needed £177.79 in May 2026 to have the same spending power of £100 in May 2006.

As such, your money needed to grow by more than three quarters (77%) during this 20-year period, just to keep pace with inflation. If it didn't. your money would have been dropping in real terms.

Having the right amount in your emergency fund and investing the rest could be a savvy move

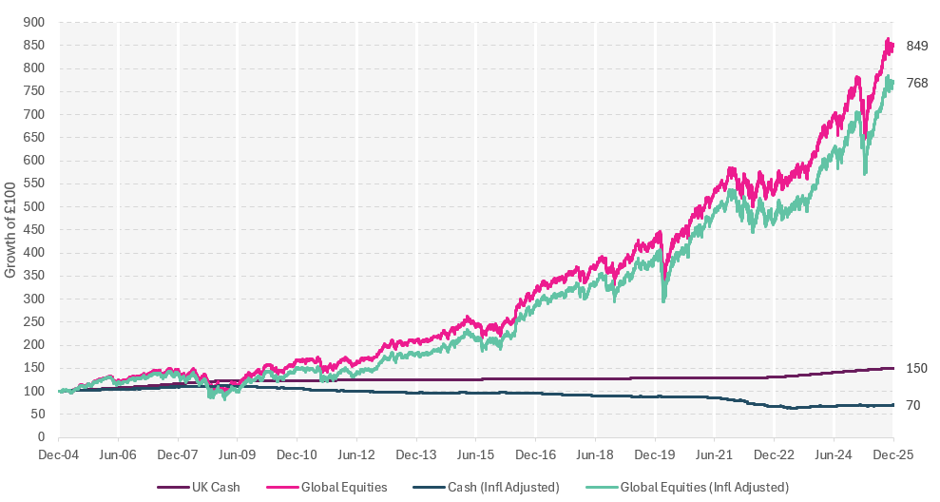

Historically, equities (otherwise known as stocks) have tended to outperform cash accounts over time. This is demonstrated in the following illustration, which shows the performance of global equities and a medium risk 60:40 multi-asset portfolio between 1 January 2005 and 31 December 2025.

Data sourced from Morningstar by AFH Wealth Management. The 60:40 portfolio allocates 60% to MSCI ACWI and 40% to Bloomberg Global Aggregate.

As you can see, the multi-asset portfolio provided significantly higher levels of growth than cash savings did during the period. This is still the case when inflation is taken into account, which means investing could help to maintain your cash’s long-term spending power.

Always remember that investing carries risk, and past performance is no guarantee of future performance. You may receive less than you originally invested.

Get in touch

Ensuring you have the right amount in your emergency fund is the bedrock of a good financial plan. As one of the UK’s largest truly independent financial advice companies, we understand this.

However, we also understand the importance of exposing your wealth to the greatest growth potential possible, at a level of risk that you’re comfortable with. That’s why our Independent Financial Advisers will work with you to create a bespoke plan that provides financial security and growth potential.

If you would like to discuss how we may be able to help you, please call us on 0333 010 0008 to arrange a no obligation initial meeting with one of our Independent Financial Advisers.

16 July 2026