Figures revealed by Auction House in May 2026 could make for interesting reading if you’re a landlord. The company, which is one of the UK’s largest residential and commercial property auctioneers, saw a 70% hike in landlords looking to sell tenanted properties in April 2026, when compared to the year before.

The reason for the increase, the property auctioneers went on to explain, was a desire to exit the rental market before the Renters’ Rights Act came into force on 1 May. The Act is the latest of a number introduced in recent years, which means being a landlord now carries major regulatory responsibility, with the additional stress and expense that this entails.

Small wonder then, that another Act could have been the final straw for many landlords. That said, the role can also provide benefits that many could find attractive.

So, what are the pros and cons of being a landlord these days? Read on to discover the considerations for and against renting properties out. Before you do though, let’s consider four regulatory changes that have increased the financial and administrative burden for landlords.

Renters’ Rights Act 2026

Under the act, which came into force on 1 May 2026, all new tenancies must be on a ‘rolling basis’ and not a fixed‑term contract, Furthermore, all new tenancies must be in writing.

In addition to this, a Renters’ Rights Act Information Sheet must be provided to tenants, which explains how the Act affects their rights. The landlord must be able to evidence that the sheet was provided.

The Act also ended ‘no fault’ evictions, meaning landlords must follow an evidence‑based legal process to regain possession of their property. Rental bidding, which is where rents are set higher than the advertised price, was also outlawed by the act.

Finally, landlords can only increase rents once a year through a statutory process and tenants will be able to appeal the increase through a tribunal system. The new regulation also prevents discrimination, which includes against pet owners.

Minimum Energy Efficiency Standards (MEES)

Rental properties must have a minimum Energy Performance Certificate (EPC) rating of E. As a result, many landlords have had to make improvements to their properties, which may be expensive.

Examples of the improvements include:

· replacing an old boiler with an energy efficient one

· fitting double glazing

· increasing loft insulation

· installing cavity wall insulation.

While properties with a poorer EPC rating can be rented out, it must be placed on the PRS Exemptions Register. Failure to meet the EPC standards could result in heavy fines.

The Government has proposed increasing the minimum EPC rating to band C by 1 October 2030, meaning landlords are being advised to aim for this level to future-proof their property. This could increase the cost of maintaining a buy to let property even further.

Health and Safety Rating System (HHSRS)

A risk-based evaluation tool that aims to make rental properties safer to live in. The tool considers 29 different types of housing hazards, to ensures properties are:

· free from mould

· not excessively cold or damp

· not a fire risk

· have proper ventilation to prevent moisture build-up.

Local authorities can use the system to force landlords to make improvements and hold them accountable for poor housing conditions.

Awaab’s Law

The law was introduced following the death of two-year-old Awaab Ishak in 2020. The toddler died of respiratory conditions after being exposed to mould in his flat for a prolonged period. Therefore, the law compels landlords to address health hazards, such as mould or excessive damp, within strict timeframes.

As you can see, Awaab’s Law and the other regulations place a significant amount of responsibility that landlords must meet and maintain. So, is being a landlord a good choice?

Ultimately it will depend on you and your circumstances, but let’s look at the potential pros and cons.

Pros

Potentially regular income

Renting property could provide a good regular income depending on how much the rent charged exceeds the mortgage (if you have one) and other costs. It’s important to remember that any earnings from your buy to let could be liable to Income Tax.

Long-term capital growth

Over the long term, UK property values have tended to increase. This is especially true in sought-after locations, or areas that have a high demand for rental properties, such as towns and cities with universities.

That said, like any investment, buying property does carry an element of risk, and you could receive back less than the amount you paid for the property.

Could protect your wealth from inflation

Rising property prices could help your wealth to rise in line with, or more than, the rate of inflation. As such, it means your money won’t be losing value in real terms against the cost of living.

Cons

Increased regulatory burden

As explained above, the Renters Rights Act and other regulations have increased the regulatory burden on landlords. Consequently, keeping on top of compliance can be time consuming and potentially expensive.

Can be mentally demanding

The responsibilities of being a landlord can be stressful, especially with the need to manage tenants and property maintenance. For example, evicting a difficult tenant could be challenging, despite the fact that you may need to service loans on the property.

Similarly, if you’re struggling to rent your property out while servicing a mortgage on it, this too could be stressful.

Increased exposure to taxes

It may be possible for landlords to deduct certain expenses from their earnings, which could help to reduce their exposure to Income Tax. That said, the income earned from rent might mean their exposure to the tax rises.

Additionally, if you earn an income from another job, the rent you receive may push you up into a higher tax bracket.

With a buy to let home, you’ll also pay the additional rate of Stamp Duty when you buy the property. This means you could be liable to a tax charge of between 5% - 17%, depending on the value it when it’s purchased.

When you come to sell the property, any gain in equity could become liable to Capital Gains Tax, which could be up to 24%.

If you sell a property, you could consider investing the equity

It’s important to speak to a tax expert and your accountant if you’re considering selling, as they’ll confirm whether it’s the right course of action for your finances. They may also be able to help reduce your exposure to tax.

If you do decide to sell your portfolio of buy to let properties, you may have a significant lump sum that you’ll then need to decide what to do with. This is where an Independent Financial Adviser can help you understand your options, and the potential opportunities and risks involved with them.

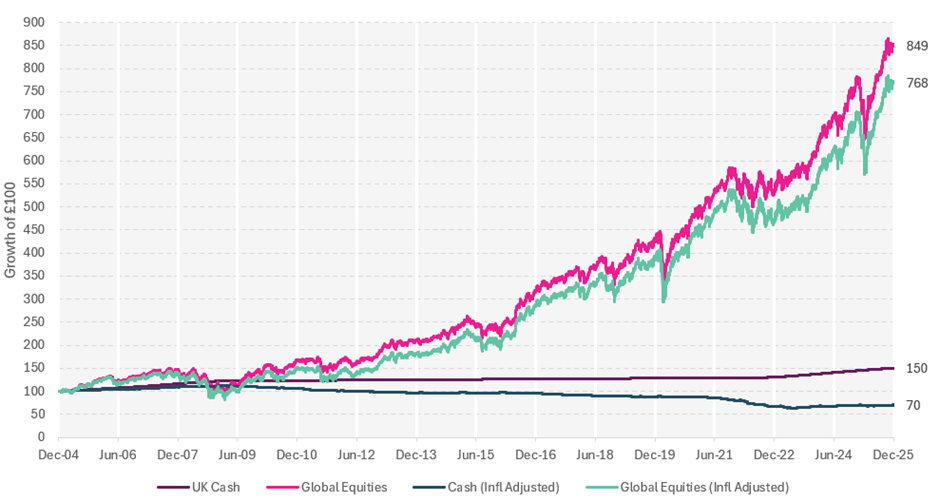

Holding the money in a savings account may seem to be the ‘safest’ option, however it could have a detrimental impact on your wealth. This is because any interest earned from savings may not keep pace with inflation over the long term, which could reduce the value of your wealth in real terms.

Investing, on the other hand, has tended to inflation-proof money over the long term. To demonstrate this, you might want to consider the following graph, which shows the performance of global equities and a medium risk 60:40 multi-asset portfolio between 1 January 2005 and 31 December 2025.

Data sourced from Morningstar by AFH Wealth Management. The 60:40 portfolio allocates 60% to MSCI ACWI and 40% to Bloomberg Global Aggregate.

As you can see, the multi-asset portfolio provided substantially higher levels of growth than cash during the period, even when inflation was factored in. This means investing the equity released from a property sale could expose it to significant growth potential over time.

Always remember that investing carries risk, and past performance is no guarantee of future performance. There is always the risk that you may receive back less than you originally invested.

Get in touch

If you would like to discuss whether investing could help to inflation-proof a lump sum from the sale of your buy to let property, please contact us on 0333 010 0008. We’d be happy to arrange a no-obligation initial meeting with one of our independent financial advisers.

13 May 2026